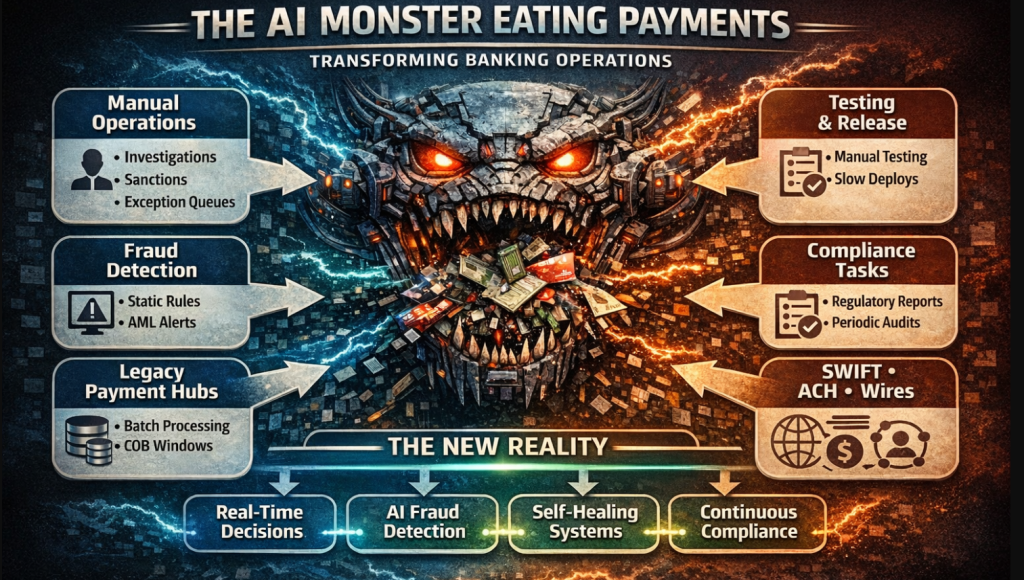

Many banks claim “AI-powered,” but the depth and quality of training data often get overlooked. What specific challenges have you faced in ensuring your models are truly robust?

Recently, Larry Ellison said AI models reach their peak value when trained on private data.

In Payment Engineering, this isn’t just true — it’s critical.

Public AI models can explain payment flows, fraud concepts, ISO standards, chargebacks, tokenization, and risk scoring. They understand theory.

But they don’t understand your transaction patterns.

They don’t know:

Your authorization rates

Your decline codes by region

Your fraud vectors

Your BIN performance

Your routing logic

Your processor latency patterns

And in payments, context is everything.

Two banks can process the same volume and have completely different fraud profiles, approval rates, and network behaviors. The difference lives in proprietary transaction data.

When AI integrates with payment data — real-time authorizations, historical declines, customer behavior, dispute history — it stops being informational and becomes operational.

It can:

Predict soft declines before they spike

Optimize routing across acquirers

Detect emerging fraud patterns unique to your system

Reduce false positives without increasing risk

Improve approval rates dynamically

The AI race in payments won’t be won by who has the biggest model.

It will be won by who leverages the richest payment transaction data.

Foundation models are becoming commoditized. Payment data is not.

Your historical payment transaction graph is unique.

Your fraud signals compound over time.

Your routing intelligence is defensible.

That’s the moat.

But private and secure data also demands discipline — encryption, compliance, PCI controls, governance. The winners will balance innovation with security.

Leave a Reply